Audit fees contribution as moderating auditor switching on audit quality: Evidence from Indonesia

Article Sidebar

Main Article Content

Abstract

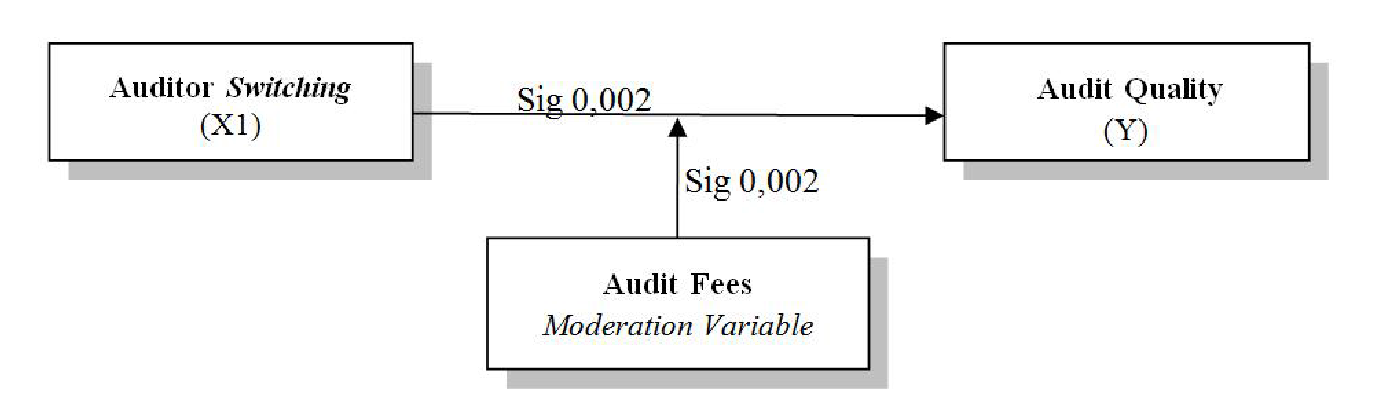

The case of an audit failure conducted by one of the KAP that occurred in Indonesia resulted in obtaining a penalty from the Public Company Accounting Overside Board (PCAOB) as the main issue in this study. Testing the effect of auditor switching on audit quality with audit fees as a moderating variable was the main objective of the study. The logistic regression method was used as an analytical tool to process data. The data used were secondary data in the form of quantitative. To get a representative sample, a purposive sampling method was used. During seven years (2012 -- 2018) of observation, 321 company data were obtained which included in the sample criteria. The data were used to be processed as research findings. The results showed that auditor switching affects audit quality and audit fees moderate the effect of auditor switching on audit quality. The contribution of this research is public accountants to be able to maintain public trust through the quality of the published audit and support the previous theory related to auditor switching, audit fees and audit quality.

Article Details

References

H. Ashari, Y. Winarto, Mitra Ernst $&$ Young Indonesia fined US$$$ 1 Million, 2017.

E. J. Aronmwan, T. O. Ashafoke, C. O. Mgbame, Audit firm reputation and audit quality, European Journal of Business and Management 5(7) (2013) 66 -- 75.

M. U. Tarigan, P. Bangun, Susanti, Effect of competence, ethics, and audit fees on audit quality, Accounting 13(1) (2013) 803 -- 832.

R. W. Scott, Financial accounting theory, Third Edition, Prentice Hall, Toronto, Canada, 2003.

M. W. Adhiputra, Effect of issuance of going concern opinions on the change of auditors in companies listed on the Indonesia stock exchange, Journal of Accounting Dynamics 7(1) (2015) 22 -- 36.

E. F. Giri, The influence of public accounting firm (Kap) tenure and Kap's reputation on audit quality: Auditor mandatory rotation case in Indonesia, National Symposium on Accounting XIII Purwokerto, (2010) 1 -- 26.

B. Hartadi, Effect of audit fee, KAP rotation, and auditor's reputation of audit quality on the Indonesia stock exchange, Equity: Journal of Economics and Finance 110 (2009) 84 -- 104.

M. Firth, O. M. Rui, X. Wu, How do various forms of auditor rotation affect audit quality? evidence from China, International Journal of Accounting 47(1) (2012) 109 --138.

M. Cameran, A. Prencipe, M. Trombetta, M. Control, Does mandatory auditor rotation really improve audit quality?, European Accounting Review 8180 (2016) 1 -- 53.

B. Pradhana, D. Saputra, Effects of audit fee, going concern, financial distress, company size, substitution of independent auditors, Accounting Journal of Universitas Udayana 3 (2015) 713 -- 729.

M. Kurniasih, R. Abdul, Analysis of factors affecting thin capitalization in multinational companies in Indonesia, Diponegoro Journal of Accounting 3 (2014) 1--10.

F. A. P. Ishak, H. D. Perdana, A. Widjajanto, Quality audit of manufacturing companies listed on the Indonesia stock exchange in 2009 -- 2013, Journal of Organization and Management 11(2) 2015) 183 -- 194.

I. K. A. Julianto, I. K. Yadnyana, I. D. G. D. Suputra, The effect of audit fee, audit planning, and audit risk on audit quality in public accounting firms in Bali, E-Business Economic Journal of Universitas Udayana 12 (2016) 4029 -- 4056.

C. K. Putri, N. Rasmini, Audit fee as a moderating effect of auditor switching on audit quality, Journal of Accounting 16(3) (2016) 2017 -- 2043.

M. C. Jensen, W. H. Meckling, Theory of the firm: managerial behavior agency and ownership structure, Journal of Financial Economics 3 (1976) 305 -- 360.

W. F. Meisser, S. M. Glover, D. F. Prawitt, Auditing and assurance services a systematic approach, McGraw-Hill Irwin, Singapore: Salemba Empat, 2006.

A. L. Watkins, W. Hillison, S. E. Morecroft, Watkids.pdf, (2004) 153 -- 193.

L. E. DeAngelo, Auditor independence, low balling, and disclosure regulation, Journal of Accounting and Economics 3(2) (1981) 113 -- 127.

W. El-Gammal, Determinants of audit fees: Evidence from Lebanon, International Business Research, 5(11), (2012) 136 -- 145.

M. O. Chandra, The effect of good corporate governance, company characteristics and KAP size against external audit fees, Journal of Business Accounting XIII(26) (2015) 174 -- 194.

P. H. Siegel, N. Mohsen, O. John, Factors influencing auditor switching in the European Union, Florida Atlantic University (2008).