On sensitivity of control chart for monitoring serially correlated data

Article Sidebar

Main Article Content

Abstract

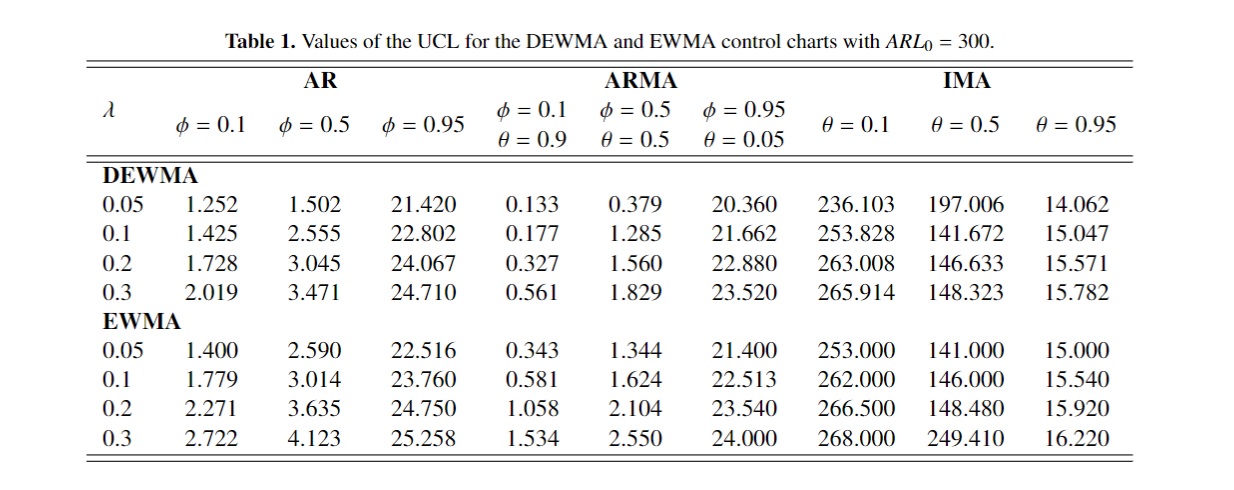

The normality and independent observations were designed for double exponentially weighted moving average (DEWMA) and exponentially weighted moving average (EWMA) control charts. DEWMA control chart was modified from the EWMA control chart. The performance of the control chart is measured in terms of the average run length (ARL) that is the average number of samples before getting an out-of-control signal. In a real application, data are dependent and non-normal observations. The exponential distribution has application in any area of the subject such as reliability theory, survival analysis and queuing theory. The purpose of this paper was to study DEWMA and EWMA control charts using the first-order autoregressive (AR(1)), the first-order autoregressive moving average (ARMA(1,1)) and the first-order integrated moving average (IMA(1,1)) models for an exponential distributed process variable to study the efficiency of detecting small process mean shift. A simulation using the R program was applied to study the ARL performances for DEWMA and EWMA control charts for the small process mean shift. Tables of ARLs are presented for the various process mean shift. All ARL at various sets of parameters of the control chart calculation was completed based on 10,000 replications for a scenario. The EWMA control chart is more efficient than the DEWMA control chart in the detection of small process mean shifts as it dependably gives smaller ARL values and quickly detects the process shift at various levels of correlation and shifts in the process mean. The application of serially correlated data in the control chart literature has achieved with wide suitability. The design and application of the DEWMA and EWMA control charts suggest a model in the detection of small process mean shift by process control employees.

Article Details

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

References

D. C. Montgomery, Introduction to statistical quality control, John Wiley & Sons, 2009.

T. J. Harris, W. H. Ross, Statistical process control procedures for correlated observations, The Canadian journal of chemical engineering 69(1) (1991) 48 -- 57.

C. H. Weib, Detecting mean increases in Poisson INAR (1) processes with EWMA control charts, Journal of Applied Statistics 38(2) (2011) 383 -- 398.

W. Suriyakat, Performance of exponentially weighted moving average control chart for exponential ARIMA processes, Far East Journal of Mathematical Sciences 100(3) (2016) 371.

S. W. Roberts, Control chart tests based on geometric moving averages, Technometrics 1(3) (1959) 239 -- 250.

P. E. Maravelakis, J. Panaretos, S. Psarakis, An examination of the robustness to non normality of the EWMA control charts for the dispersion, Communications in Statistics-Simulation and Computation 34(4) (2005) 1069 -- 1079.

S. E. Shamma, A. K. Shamma, Development and evaluation of control charts using double exponentially weighted moving averages, International Journal of Quality & Reliability Management 9(6) (1992).

S. M. M. Raza, M. Riaz, S. Ali, On the performance of EWMA and DEWMA control charts for censored data, Journal of the Chinese Institute of Engineers 38(6) (2015) 714 -- 722.

S. M. M. Raza, A. F. Siddiqi, EWMA and DEWMA Control Charts for Poisson?Exponential Distribution: Conditional Median Approach for Censored Data, Quality and Reliability Engineering International 33(2) (2017) 387 -- 399.

S. M. M. Raza, S. Ali, M. M. Butt, DEWMA control charts for censored data using Rayleigh lifetimes, Quality and Reliability Engineering International 34(8) (2018) 1675 -- 1684.

P. J. Brockwell, R. A. Davis, M. V. Calder, Introduction to time series and forecasting (Vol. 2), New York: springer 2002.

J. Andel, On AR (1) processes with exponential white noise, Communications in Statistics-Theory and Methods 17(5) (1988) 1481 -- 1495.

M. A. Amaral Turkman, Bayesian analysis of an autoregressive process with exponential white noise, Statistics 21(4) (1990) 601 -- 608.

H. Fellag, M. Ibazizen, Estimation of the first-order autoregressive model with contaminated exponential white noise, Journal of Mathematical Sciences, 106(1) (2001) 2652 -- 2656.

M. Ibazizen, H. Fellag, Bayesian estimation of an AR (1) process with exponential white noise, Statistics 37(5) (2003) 365 -- 372.

M. B. Vermaat, F. H. Van der Meulen, R. J. M. M. Does, Asymptotic behaviour of the variance of the EWMA statistic for autoregressive processes. Statistics & Probability Letters 78(12) (2008) 1673 -- 682.

R Core Team R: A language and environment for statistical computing, R Foundation for Statistical Computing, Vienna, Austria, Available from: https://www.R-project.org/. (accessed 2017).