Stock Price Prediction of TLKM and BBCA Using SVR, Random Forest, and LSTM

Article Sidebar

Main Article Content

Abstract

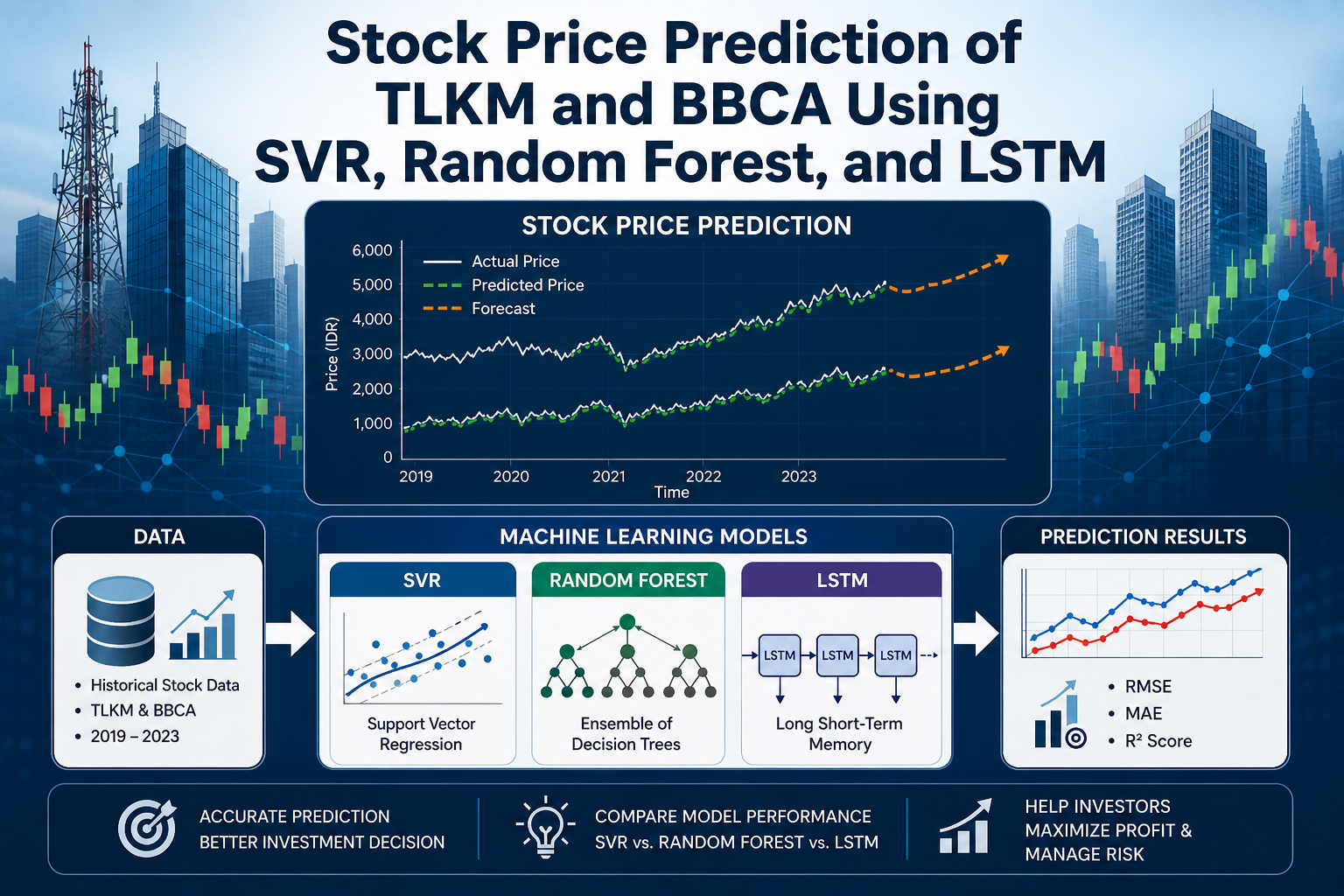

Stock price prediction is a significant challenge in financial market analysis due to the influence of many dynamic and nonlinear factors. This study compares three machine learning methods, namely Support Vector Regression (SVR), Random Forest (RF), and Long Short-Term Memory (LSTM), in predicting the stock prices of PT Telekomunikasi Indonesia Tbk (TLKM) and PT Bank Central Asia Tbk (BBCA) for the period 2019–2023. Data were obtained from Yahoo Finance (15). Model Performance Comparison for TLKM Stock, the testing results show that LSTM achieved RMSE of 0.040093, MAE of 0.029849, and R² of 0.905330, indicating the best performance compared to SVR and Random Forest. Random Forest had an RMSE of 0.138295 and an MAE of 0.114423, while SVR had the highest RMSE at 0.238130. Model Performance Comparison for BBCA Stock: The testing results show that LSTM achieved RMSE of 0.055023, MAE of 0.048056, and R² of 0.657730, indicating the best performance compared to SVR and Random Forest. Random Forest had an RMSE of 0.252568 and an MAE of 0.236129, while SVR had the highest RMSE at 0.6211363. This confirms the LSTM model's effectiveness in capturing temporal patterns in stock data (5), (9), (13).

Article Details

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.

References

Kumar, R.; Saini, N. Data Preprocessing and Normalization in Stock Market Prediction Using Machine Learning. Procedia Comput. Sci. 2021, 184, 123–130. https://doi.org/10.1016/j.procs.2021.03.022

Rahman, M.; Chowdhury, S.; Akter, F. Comparison of SVR, Random Forest, and LSTM Models for Stock Price Prediction. Int. J. Data Sci. 2022, 9(1), 67–79.

Chen, J.; Yang, H. Deep Learning Architectures for Stock Price Forecasting: A Comparative Analysis. J. Financ. Data Sci. 2022, 4(3), 45–59.

Nguyen, T.; Tran, L. Machine Learning in Stock Prediction: A Review of Methods and Applications. Appl. Intell. 2023, 53(8), 987–1003. https://doi.org/10.1007/s10489-022-03845-9

Li, P.; Wang, X.; Zhang, Y. Long Short-Term Memory Networks for Financial Time Series Forecasting. Expert Syst. Appl. 2023, 224, 119137. https://doi.org/10.1016/j.eswa.2023.119137

Putra, D.; Simanjuntak, E.; Ginting, M. Analysis of Stock Prediction in the Telecommunications Sector Using Machine Learning. J. Teknol. Inf. Keuang. 2023, 12(2), 87–96.

Zhang, W.; Liu, Y.; Chen, L. Stock Market Forecasting Using Hybrid Deep Learning Models. IEEE Access 2022, 10, 55132–55145. https://doi.org/10.1109/ACCESS.2022.3187511

Smith, A.; Jones, B. Ensemble Methods for Stock Price Volatility Prediction: Random Forest Enhanced. Financ. Eng. Rev. 2024, 15(1), 32–47.

Hernandez, R.; Garcia, M. Time Series Data Augmentation in Finance: Improving LSTM Predictions. J. Comput. Financ. 2024, 12(2), 102–118.

Oliveira, F.; Santos, P. Comparative Study of Machine Learning Methods for Stock Trend Forecasting. Int. J. Financ. Stud. 2021, 9(4), 70.

Kim, S.; Lee, H. Feature Engineering Impact on Deep Learning-Based Stock Forecasts. Data Min. Appl. Financ. 2023, 7(3), 210–223.

Chen, Y.; Martin, A.; Brown, K. Evaluating SVR Performance on Financial Time Series: A Case Study. Appl. Soft Comput. 2022, 115, 107123. https://doi.org/10.1016/j.asoc.2022.107123

Wang, Z.; Xu, L. Predicting Stock Returns with Deep Learning and Technical Indicators. J. Financ. Data Sci. 2023, 9, 45–58.

Tan, J.; Ho, L. Real-Time Prediction of Stock Prices Using LSTM and Attention Mechanisms. Comput. Econ. 2024, 63, 789–807.

Yahoo Finance. Historical Data of TLKM.JK and BBCA.JK; 2024. Available online: https://finance.yahoo.com